In some countries like the US the tax system is bracketed rather than continuous.

There would be some obvious trade offs, but would it be worth considering eliminating the marginal, bracketed tax system in favor of a continuous, non-marginal tax rate system without brackets?

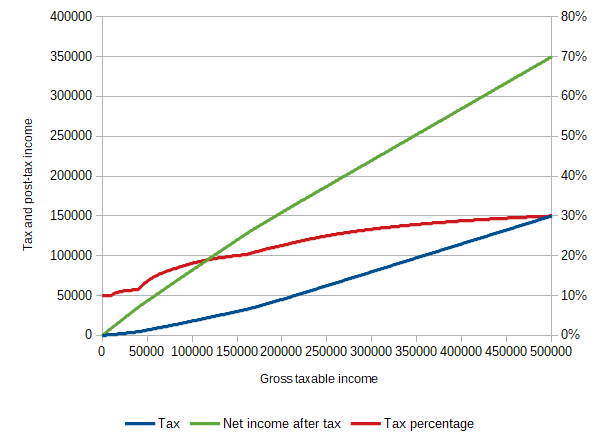

Picture a chart with income on the X axis and tax rate on the Y axis. In the current bracketed tax system the tax rate line increases as steps in a ladder. In a continuous tax system the tax rate would instead increase along some line or curve as income increased. This would shift the tax debate from,

“Where should we place the brackets and how many brackets should there be?”

to

“Where should the line or curve start and how fast should it rise?”

Update

Thank you to all who have taken time to propose answers and comment so far. Your tremendous feedback unburdened some of my misunderstandings and helped me recognize some confusing points and distractions in how the original question was posed. To that end I offer this attempt to clarify the question.

The focus of the question was intended to be a generic comparison of bracketed vs continuous systems that ignores whether the bracketed system is marginal. However, I don’t know enough about tax systems to know if any relevant bracketed tax systems are non-marginal. As such, despite the discussion of incentives in the original question, non-marginal bracketed tax systems were not intended to be the focus of the question.

In an attempt to avoid this confusion I’ve updated the text in the question above to reduce the scope of the question such that it includes only the comparison between bracketed, marginal tax systems versus continuous, non-marginal, non-bracketed tax systems.

Also, the wording of my original question included possible incentives for earners to not pass an income bracket. This wording understandably caused some answers to focus on an implied misunderstanding of marginal brackets. Even in the cases where bracketed tax systems are marginal I think some incentives (real or perceived) for an earner not passing a bracket could exist. However, given that any possible incentives for avoiding crossing a tax bracket are a minor point and not the focus of the question, I’ve moved this discussion from the question’s introduction to the “Assumptions” section below.

With these clarifications in mind please also note that I know next to nothing about tax systems. Where you notice an error in the following assumptions, please point them out and I will try to update to help others.

Assumptions

Rightly or wrongly, the following aspects of a bracketed, marginal tax rate system may seem confusing, be perceived as unfair, or disincentivize earning for some people in some cases:

There seems to be a common public misunderstanding of how marginal tax brackets work. For example, the belief that earning into the next bracket may subject a person’s entire income to that bracket’s tax rate rather than just the amount earned within the bracket. For people who have such a misunderstanding, they may be reluctant to earn into the next tax bracket in order to avoid what they think will result in significantly higher taxes across their entire income.

For those who do understand how the marginal system works, earning just under each bracket may still have a perceived advantage over going over a bracket in some cases. For example, while likely a minor concern, if the tax rate for the next bracket is believed to be significantly higher then the final tax percentage for all earnings may be seen to increase disproportionately for the amount earned when going over the next bracket.

There may be cases where a discrete, all or nothing tax incentive is offered only to those whose earnings do not reach the next bracket. While tax incentives won’t necessarily have a 1 to 1 mapping to a tax bracket, this may happen for simplicity in some marginal tax systems.

Calculating the base taxes owed (before applying tax incentives, loopholes, etc.) requires summing the taxable area under each bracket by first knowing the tax rate for each bracket where earnings were made, determining the amount earned within each bracket, multiplication of the rate and the total earnings for each bracket, summing each bracket’s taxable income with taxes owed for all the other relevant brackets, etc. While these calculations aren’t difficult, per se, they may require additional tax resources and make the system feel more complicated than necessary for some people – especially when brackets boundaries or their tax rates change.

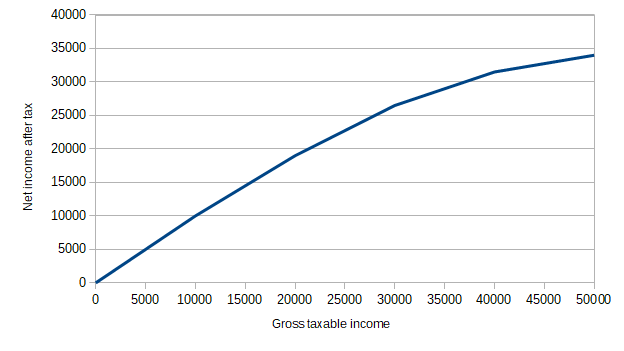

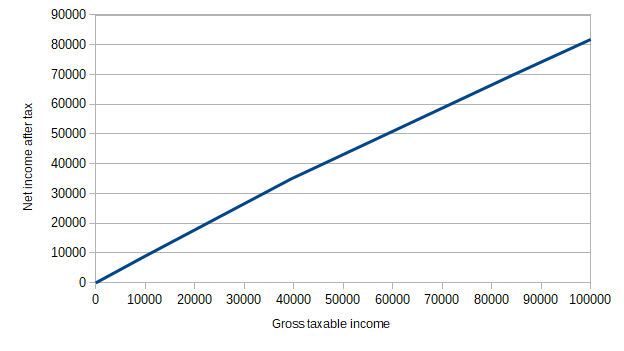

A continuous, non-marginal tax rate system without brackets would surely have it’s own set of problems but it would seem to avoid all points listed above. For example, as opposed to 1-4 above, in a continuous, non-marginal tax rate system without brackets:

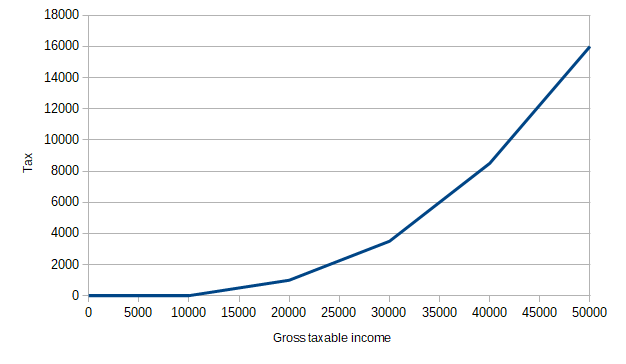

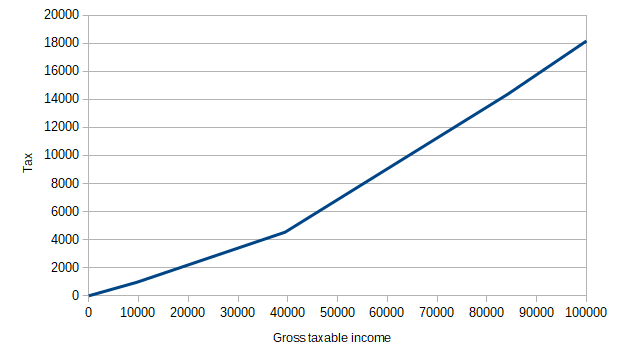

The public would be more likely to intuitively understand their tax rate because it is in line with what they expect when they hear “tax rate for X income is Y percent”. For example, they could find their income on the tax chart (a continuous curve) to find their tax rate. Multiplying their income by the percentage on the chart would yield their base taxes owed before any tax incentives are applied. There would be no need to use complex maths like calculus to derive the area under the curve because the continuous tax system in question is not marginal.

Since the tax rate change is continuous there would be no specific point in the curve that could be seen to disproportionately increase the final tax percentage.

While point 3 above could happen in a continuous system as well depending on how the tax laws are written, a continuous system would be more likely to change the way politicians communicate and how legislation creates tax incentives such that they would begin to apply in a continuously increasing or decreasing income range rather than applying in an all or nothing fashion at income X. This may cause the public to view the tax system as more fair.

Determining the taxes owed (at a base level prior to any incentives, loopholes, etc.) would only require knowing the single tax percentage for the earned income in question. This would ease the burden on communication resources required to help the public determine their base tax rate prior to specific tax incentives.

While a continuous, non-marginal, non-bracketed tax rate system seems like it may be perceived to be more fair and easier for the public to understand it would certainly have serious negative trade offs worth discussing. This was the impetus and background for the original question and should be seen as context for the question as posed above.

Discrete brackets may also disincentivize earnings in some situations if an individual is just below a bracketThat's a misunderstanding of how marginal tax rates work. Having a higher income will never result in less money (at least at far as the tax system is concerned).