Increasing corporate tax rates from 21% to 35%, undoing the tax rate cut in the 2017 tax act would raise about $249 billion a year. U.S. C-corporations paid $374 billion of corporate income taxes in 2020 at a flat corporate income tax rate of 21% from $2,700 billion of corporate net income, reduced by $193 billion of corporate tax credits. Corporate profits predominantly benefit the top 1%.

The end of the tax treatment of capital gains would increase federal tax revenues by $162 billion, and the end of favorable taxation of qualified dividend would increase federal tax revenues by about $84 billion; allowing the deduction for 20% of pass through entity income to expire would increase tax revenues by about $55 billion a year. (Source) The pass through entity deduction dates to the 2017 Tax Act. The qualified dividends tax rule taxes to the 2003 Tax Act. The favorable treatment of capital gains dates to a few years after the 1986 tax reform, which briefly taxed capital gains as ordinary income.

These changes would raise $550 billion a year.

The annual budget deficit is about $1,200 billion a year, so the increased taxes would reduce it by about 46%.

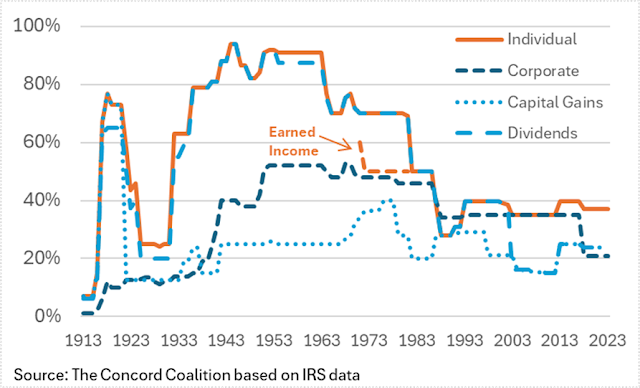

Other tax tweaks rolling back tax breaks created after the early 1990s could raise even more, predominantly from the top 1%.

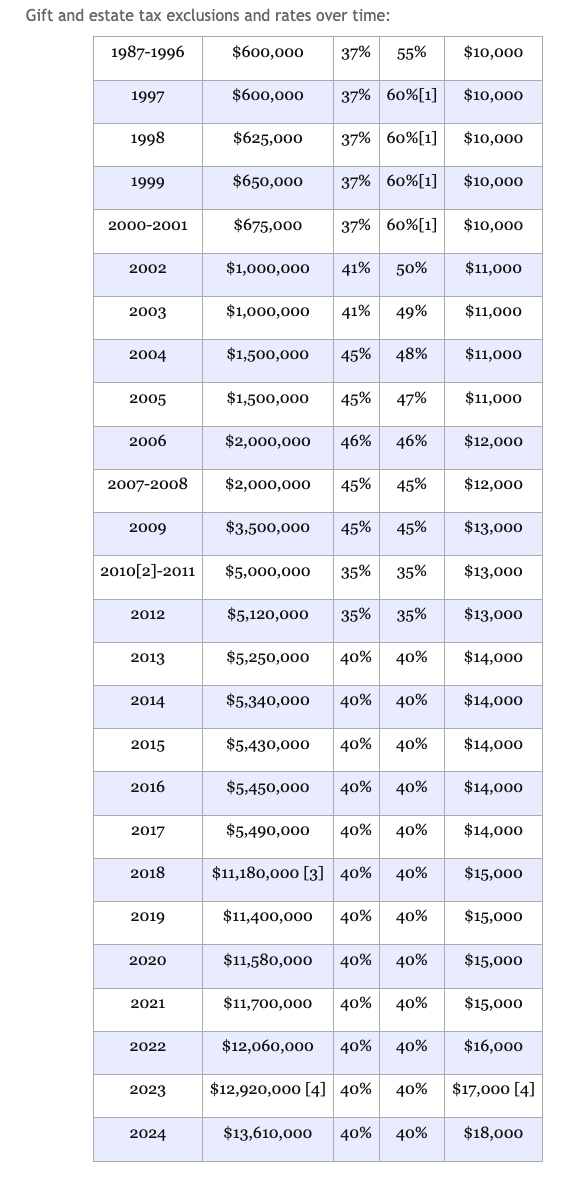

For example, the amount of gift and estate taxes imposed in the early 1990s on the top 1% was much greater than it is today (on a percentage basis).

The top 1 percent earned 26.3 percent of total AGI and paid 45.8 percent of all federal income taxes at an average income tax rate of individual income of about 26% (excluding corporate income imputed to owners of corporations). Total individual income taxes in 2021 were about $2,200 billion on $14,700 billion of individual adjusted gross income. (Source)

One could, at a minimum, easily reduce the deficit by 50% by rolling back tax breaks that predominantly benefit the top 1% to early 1990s levels.

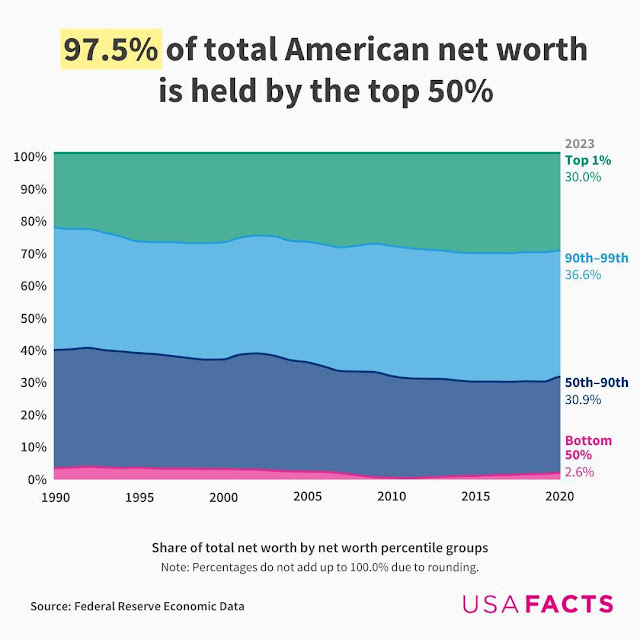

The wealth and income needed to generate this income is there: