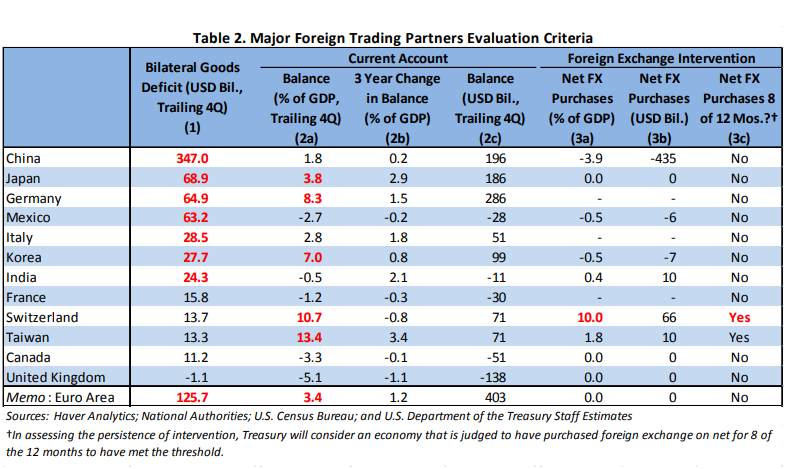

The criteria that the US Treasury applies to label a currency manipulator, according to US law

Criterion (1) - Significant bilateral trade surplus with the United States. Treasury assesses that economies with a bilateral goods [...]

surplus of at least $20 billion (roughly 0.1 percent of U.S. GDP) have a “significant” surplus.

Criterion (2) – Material current account surplus. Treasury assesses current account surpluses in excess of 3 percent of GDP to be “material”

for the purposes of enhanced analysis. Highlighted in red in column 2a are the five

economies that had a current account surplus in excess of 3 percent of GDP for the four

quarters ending December 2016. In the aggregate, these five economies accounted for

more than half of the value of global current account surpluses in 2016. Column 2b shows

the change in the current account surplus as a share of GDP over the last three years,

although this is not a criterion for enhanced analysis.

Criterion (3) – Persistent, one-sided intervention:

Treasury assesses net purchases of foreign currency, conducted repeatedly, totaling in

excess of 2 percent of an economy’s GDP over a period of 12 months to be persistent, one-sided

intervention. Columns 3a and 3c in Table 2 provide Treasury’s assessment of this

criterion. In economies where foreign exchange interventions are not published, Treasury

uses estimates of net purchases of foreign currency to proxy for intervention. Switzerland

meets this criterion for the last four quarters available, per Treasury estimates.

Pursuant to the 2015 Act, Treasury finds that no major trading partner of the United

States met all three criteria in the current reporting period. Five major trading partners of

the United States, however, have met two of the three criteria for enhanced analysis in this

Report or in the October 2016 Report. Additionally, one major trading partner, China,

constitutes a disproportionate share of the overall U.S. trade deficit. These six economies –

China, Japan, Korea, Taiwan, Germany, and Switzerland – constitute Treasury’s Monitoring

List. Japan, Germany, and Korea met two of the three criteria in both the October 2016

Report and this Report, having material current account surpluses combined with

significant bilateral trade surpluses with the United States. Switzerland met two of the

three criteria in both the October 2016 Report and this Report, having a material current

account surplus and having engaged in persistent, one-sided intervention in foreign

exchange markets. Taiwan met two of the three criteria in the October 2016 Report –

having a material current account surplus and having engaged in persistent, one-sided

intervention in foreign exchange markets – and it met one of the three criteria in this

Report, a material current account surplus. [...] China met only one of the three criteria in this Report, a large bilateral trade

surplus with the United States, but this surplus accounts for a disproportionate share of the

overall U.S. trade deficit.

Some more relevant quotes from the 2017 US Treasury report:

Germany, the largest economy within the euro area, should take policy steps –

particularly greater use of fiscal policy – to encourage stronger domestic demand

growth, which would place upward pressure on the euro’s nominal and real effective

exchange rates and help reduce its large external imbalances. [...]

The European Central

Bank (ECB) has not intervened in foreign currency markets since 2011, and did so then

as part of a G-7 concerted intervention to stabilize the yen following Japan’s earthquake and tsunami.

In other words, the Fed thinks [some of] the eurozone should give itself a stimulus (e.g. tax cut) as to lead to rise in the value of the euro (relative to the dollar). And then the Fed acknowledges the heterogeneity of the eurozone, only to circle back on Germany:

Persistent weaknesses in some of the peripheral euro area economies,

including Greece, Italy, and others, have contributed to uncertainty about the resilience of

the monetary union and have effectively weakened the euro over the last several years,

both against the dollar and on a nominal and real effective basis. Euro area monetary

policy has had an effect as well, as easing by the ECB has opened a sizable gap in interest

rates and bond yields between the United States and the euro area.

The combination of a relatively weak currency plus weak domestic demand (averaging just

0.5 percent per year the last six years), has led to a significant widening of the euro area’s

current account surplus from 0.2 percent of GDP in 2009 to 3.4 percent in 2016. Much of

this has been driven by a rapid increase in Germany’s surplus, which is now the largest

nominal surplus in the world at $287 billion. Germany’s real effective exchange rate has

depreciated by 10 percent since 2009, a shift that would be counterintuitive in light of

Germany’s large and persistent current account surplus but for its membership in the

monetary union. [...]

Germany’s bilateral trade surplus with the United States is also very sizable and a matter of

concern for Treasury. Treasury recognizes that Germany does not exercise its own

monetary policy and that, in the absence of stronger growth elsewhere in the currency

union, upward pressure on the nominal and real effective exchange rates may not be strong.

Treasury also recognizes that Germany is near full employment. Nevertheless, Germany

has a responsibility as the fourth largest global economy and as an economy with a very large external surplus to contribute to more balanced demand growth and to more

balanced trade flows. Pushing demand against inelastic supply will help push up wages,

domestic consumption, relative prices against many other euro area members, and demand

for imports, and will help appreciate Germany’s low real effective exchange rate. This

would contribute to both global and euro area rebalancing.

So again, the Treasury says Germany needs a stimulus to its (internal) demand.

Also note that India was added to the Monitoring list as well, this year, again for meeting two of tree criteria (the fist and the 3rd.)

Also the relevance of the first criterion is disputed by other (US) economists, e.g. those of PIIE:

Treasury limits its analysis to the top 12 trading partners, and, as required by statute, includes a criterion that a country have a significant bilateral trade surplus with the United States. However, with today's mobile capital and complex supply chains, bilateral trade balances are not an appropriate criterion for manipulation.

And they have a more elaborate list of criteria, (two of which overlap with the [latter two] non-disputed ones the Treasury applies). According to the more elaborate criteria, the picture looks pretty different:

But most of the EU is not there. Norway is only an EEA member; Norway also has its Norwegian krone as its national currency.

And regarding the US Treasury definition, an article in The Economist also claims that there's some kind of consensus the statutory criteria used by the Treasury is inadequate:

America’s Treasury makes a six-monthly assessment of the foreign-exchange policies of its big trading partners. The criteria it uses to identify currency manipulators are regarded by many economists as inadequate. They do not include, for example, the domestic purchasing power of a currency. [...]

But then the Economist indulges the Treasury's method, with a twist similar to PIIE's:

Using the current-account metric, we award one “manipulation point” to countries with surpluses at the 3% threshold, two points to economies with surpluses at 6% of GDP, and so on. Similarly, we award one manipulation point for each 2% of GDP spent buying foreign assets to depress the value of its currency. We do not include bilateral trade with America in the scoring: the value of currencies affects trade globally, and some countries such as Mexico run hefty trade surpluses against America but have deficits with the rest of the world.

Awkwardly for America, two of its friends in Asia have recently scored more highly than China: South Korea and, most clearly, Taiwan. But the highest score of all goes to Switzerland, by dint of its whopping current-account surplus and its hefty foreign-currency purchases. This illustrates one of the method’s flaws: in terms of the goods and services that it can actually buy, the Swiss franc is in fact among the world’s most overvalued currencies.

Germany is not mentioned in the text there, but it does show in the graph (with a fairly low manipulation level, roughly on par with South Korea's):

A Rice University discussion paper on the topic of currency manipulation further notes that although both the IMF and the US Treasury have rules or thresholds for currency manipulation, these have seldom led to action:

The IMF only started talks on two countries: Sweden in 1982 and South Korea

in 1987.

The US has labelled 3 countries (in 4 cases) as outright manipulators (i.e. meeting all criteria): Taiwan and South Korea in 1988, and

China and Taiwan in 1992.

The paper also notes that

Identifying the intent of government action

becomes extremely difficult because

domestic policy and exchange rate policy

are intrinsically intertwined. With few

exceptions, attempts to distinguish between

the two are fruitless. [...]

Since 2013

the IMF has used three different indicators

of exchange rate misalignment, two

statistical and the third judgmental. This

measure improves upon the previous

methodology developed only five years

prior. The multiplicity of measures and their

frequent revisal leaves plenty of room for

debate. Even when all three of the current

IMF indicators point in the same direction,

countries disagree with IMF assessments.

Identifying misalignment leads

to the next, even messier question of

intent. Because domestic policies can

move exchange rates, countries pursuing

legitimate domestic goals may invite

accusations of currency manipulation.

Indeed, this is one major concern raised by

Janet Yellen, chair of the US Federal Reserve,

in opposing the idea of a currency chapter.

Of course, the opposite is also possible. A

country intending to manipulate its currency

for unfair trade advantage may use domestic

policy levers to do so, obscuring its intent.

Either case leads to a debate about the

legitimacy of purported domestic objectives.

No precedent exists for resolving such a

debate in an objective fashion. IMF policy

is to give the benefit of the doubt to the

country enacting the policy.

Case in point: the "Statement by Mr. Merk, Alternate Executive Director on Germany, June 29, 2018" at the end of IMF's most recent assessment of the German economy:

My authorities reiterate their view that the German current account surplus is a result

of private sector decisions in international trade as well as in domestic saving and

investment and not of domestic policy distortions. To a considerable degree the current

account surplus is explained by the rapidly aging population. Therefore, we expect that the

current account surplus will decline in the years to come, especially when the baby boomers

will retire. Also, differences in expected GDP growth domestically and abroad and trading

partners’ policies help explain the surplus. It is not fully clear whether these factors are

adequately reflected in the models used by the staff to evaluate current account balances.

Therefore, we would like to stress that a cautious interpretation of EBA “norms” is

warranted, given the high model and estimation uncertainty. The same is true for the REER

estimates: In contrast with the IMF assessment, the Bundesbank currently does not consider

the REER as significantly undervalued, and instead assesses German price competitiveness

to be neutral within reasonable error bounds. Methodically, we would reiterate the view that

on a global scale – since Germany is a member of the European Monetary Union – the euro

area balance should be the primary reference for assessing the significance of current account

developments.

Which seems to be taking issue with the following paragraph from the IMF staff's assement:

Germany’s external position remains substantially stronger than implied by medium-term

fundamentals and desirable policy settings. The cyclically adjusted CA [current account] surplus stood at

8¼ percent of GDP in 2017, modestly lower than in 2016 and 3¼–6¼ percent of GDP above the

interval assessed as being consistent with economic fundamentals and desirable policy settings of

2–4½ percent of GDP (the norm). The estimated norm is somewhat lower than in previous years,

due to refinements to the Fund’s External Balance Assessment model and data updates. Part of the

resulting CA gap (0.8 percentage point of GDP) is attributed to domestic policy distortions:

0.4 percentage point is due to domestic fiscal policy and 0.4 percentage point is due to the low

credit-to-GDP ratio in Germany, which partly reflects relatively low investment (Annex VIII). The real

effective exchange rate (REER) is estimated to remain undervalued by 10–20 percent, consistent with

the large current account gap.

(As I noted already, Germany disagrees with this IMF assessment.)

Paul Krugman has also chimed on whether Germany is a currency manipulator:

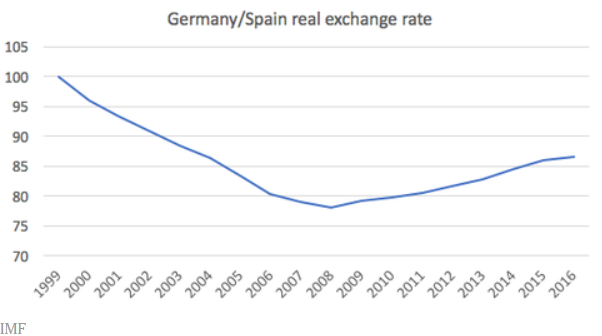

Yes and no. Unfortunately, the “no” part is what’s relevant to the US.

Yes, Germany in effect has an undervalued currency relative to what it would have without the euro. The figure [below] shows German prices (GDP deflator) relative to Spain (which I take to represent Southern Europe in general) since the euro was created. There was a large real depreciation during the euro’s good years, when Spain had massive capital inflows and an inflationary boom. This has only been partly reversed, despite an incredible depression in Spain. Why? Because wages are downward sticky, and Germany has refused to support the kind of monetary and fiscal stimulus that would raise overall euro area inflation, which remains stuck at far too low a level.

So the euro system has kept Germany undervalued, on a sustained basis, against its neighbors.

But does this mean that the euro as a whole is undervalued against the dollar? Probably not. The euro is weak because investors see poor investment opportunities in Europe, to an important extent because of bad demography, and better opportunities in the U.S.. The travails of the euro system may add to poor European perceptions. But there’s no clear relationship between the problems of Germany’s role within the euro and questions of the relationship between the euro and other currencies.

And may I say, what is the purpose of having someone connected to the U.S. government say this? Are we going to pressure the ECB to adopt tighter monetary policy? I sure hope not. Are we egging on a breakup of the euro? It sure sounds like it — but that is not, not, something the US government should be doing. What would we say if Chinese officials seemed to be talking up a US financial crisis? (It would, of course, be OK with Trump if the Russians did it.)

And Krugman is fairly correct IMO in saying that if the (say) the German (never mind the Chinese) government started making recommendations on US fiscal or monetary policy... people would be appalled, especially in the US.

PIIE also also has a (longer) take on this German issue, from which I found this bit interesting becase it puts the current situtaion in the eurozone in historical perspective:

Germany chose to adopt the euro more than 20 years ago. Its motive was not to enhance German competitiveness but to strengthen European economic and political integration. Like all other euro members, Germany entered the currency union at the—unmanipulated—market exchange rates prevailing at the time. In fact, the initial consequence of euro membership was not to make Germany more competitive. Quite the reverse: Because of north-south capital flows and faster productivity growth in the poorer euro member countries, Germany quickly became overvalued within the euro area, triggering a recession in 2003. The euro’s undervaluation today is largely a consequence of the euro crisis. So the assertion that German euro membership constitutes currency manipulation is baseless for two reasons: Euro membership did not reflect any decision, on behalf of the German government, to steer its exchange rate in any particular direction. Nor is Germany’s competitiveness a structural feature of euro membership. Euro membership merely implies that the real exchange rate—Germany’s price level relative to others, expressed in a common currency—takes longer to adjust to shocks and crises than would be the case in a floating system. [...]

The United States has complained about the German current account surplus for years, and so has the European Commission. The result of these [latter] complaints has been a set of [EU] policy recommendations directed at Germany.

(The German recession from 2003 is not a typo.)