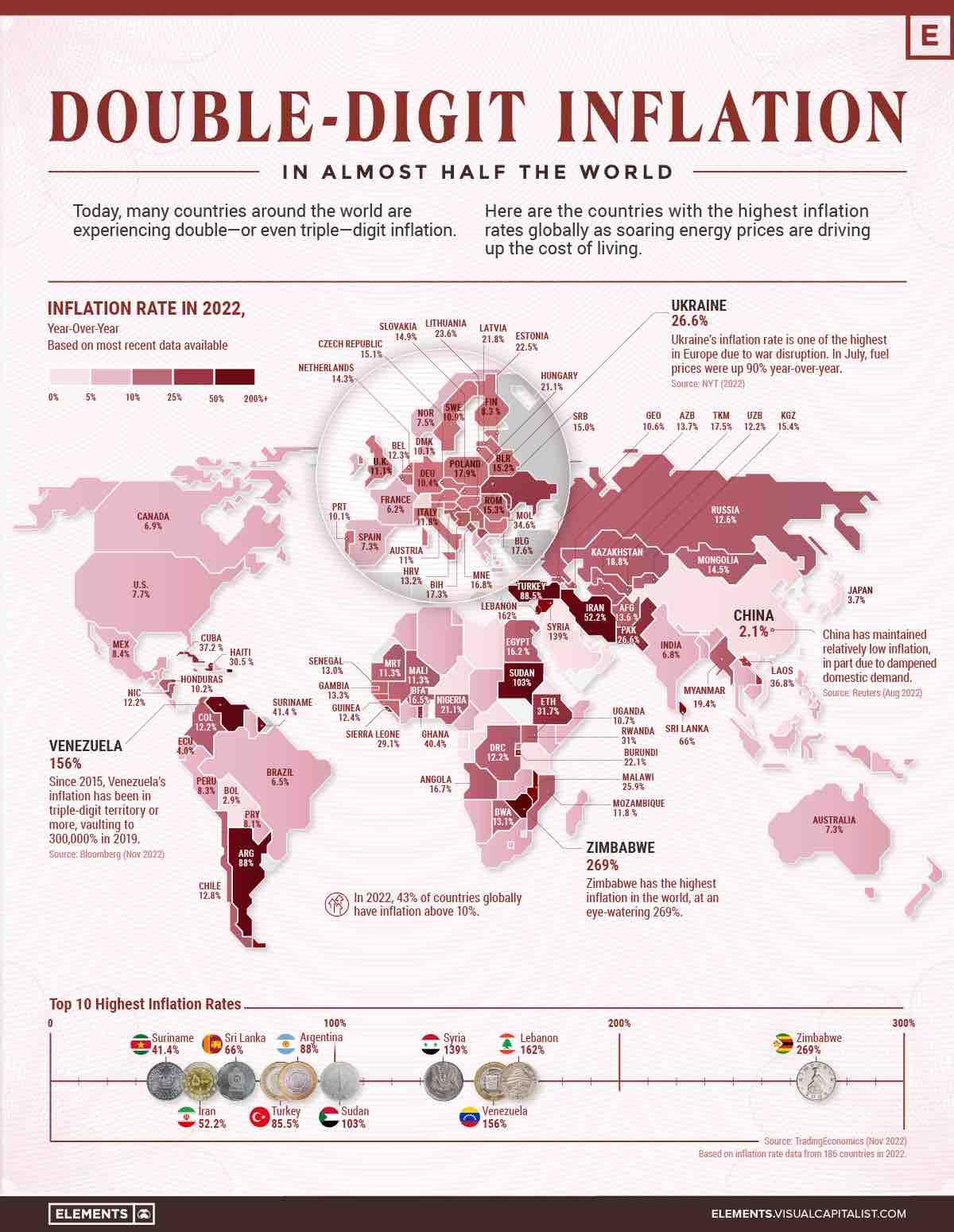

According to the IMF (or at least according one of their economists), food and energy prices were main drivers of inflation in 2022, worldwide. (Now the real/tough question is how much of the latter was due to the war between Russia and Ukraine.) But if one is be more accurate, slightly less than half of the inflation is due to energy & food, the rest is due to "unexplained" factors, which is one way to say typical economic models aren't too good at capturing those causes. But from the same (IMF) source, the UK saw a higher than average impact of the "heating crunch", i.e. higher price increase than in most of Europe for heating. So, if you're willing to concede the war had something to do with that, the UK was seemingly affected more than other European countries, at least on those energy prices.

One aspect that's alas not touched in that IMF analysis are gov't efforts this year to subsidize/cushion the impact by absorbing some of the price increases. I suspect (but don't have data immediately on hand) that such mitigations might have been higher [e.g.] in Germany (than in the UK), for instance. Such interventions would reduce inflation growth short term, but there's no free lunch here, as increasing public debt etc. may well have a delayed effect.

There's some data in the Guardian that qualitatively suggests Germany might a have done a bit more, i.e. cut some energy taxes, but both Germany and the UK gave some flat subsidies to the poorest households. (Alas it's not terribly easy to compare the overall magnitude of those packages, or their impact on inflation.)

CNN also ran a piece in August, titled "Why UK energy prices are rising much faster than in Europe". Those numbers might a bit dated by now, but expectations (at least based on Deutche Bank modelling) back then were that

"Annual consumer price inflation for gas and electricity in the United Kingdom is forecast to soar to an average of around 80% this year, compared to an average of 40% across the 19 countries that use the euro." That analysis points to the higher passthrough of energy production prices onto consumers in the UK. Depending where you stand on the economic libertarianism scale, that could be good or bad (i.e. you can read it as a more flexible market), but the short term effects of such generally are higher swings in case of shocks.

So this is not really an easy question to answer. There's an interaction between shocks and what economists call structural factors.

It's also worth noting that before the war had a chance to have much of an impact on markets, i.e. around March 2022, the UK already had higher inflation than France or Germany. Back then, some economists were pointing to Brexit as a contributing factor, both on labor market front and [new] trade barriers.

I don't want to wade into the Covid [restrictions] discussion much (IIRC they were mostly gone in Europe in 2022), but some sources note that due to China's prolonged "zero Covid" policy in 2022 (only recently abandoned), an effect of that has been "reduced" energy demand in China, so the effect of those Covid restrictions reflected on Europe's inflation, at least energy-wise, might actually have been to mitigate rather than increase inflation. (TBH, this argument is slightly misleading/misstated, as such. What happened in pure quantitative terms is that China's energy demand grew less in 2022 compared to the previous year, i.e. 3.6% vs 10.3% increase. So, it's only a decrease in those terms, i.e. less of an increase than one might have expected.) On the other side of the coin, there are the various supply chain disruption for various other goods that reduced production [increase] in China entailed. (There's also a somewhat interesting analysis that concludes that China's business cycle has become somewhat desynchronized from "the West", since the pandemic. And this observation holds in terms of inflation too; see fig 1. in that paper.)

However one shouldn't discount too much the cumulative and delayed effects of these Covid-related disruptions, e.g. and IMF cross-countries study from March last year (conducted before the war was having much of an effect), concluded that "when freight rates double, inflation picks up by about 0.7 percentage point. Most importantly, the effects are quite persistent, peaking after a year and lasting up to 18 months. [... On the other hand] the pass-through to inflation is less than that associated with fuel or food prices—which account for a larger share of consumer purchases".